Audit

We conduct statutory audits (audits required by law) and voluntary audits (audits requested by management, etc. that are not required by law).

Statutory audits Example

- Auditing of large companies based on the Companies Act

- Auditing of private schools based on the Private School Promotion Subsidy Law

- Statutory audits of independent administrative agencies based on the Act on General Rules for Independent Administrative Agencies

- Statutory audit of national university corporations based on the National University Corporation Law

- Statutory audits of local independent administrative agencies based on the Local Independent Administrative Agency Law

- Statutory audits of public interest associations, public interest incorporated foundations, and general associations and general incorporated foundations

- Statutory audits of social welfare corporations based on the Social Welfare Law

- Statutory audits of social medical corporations and medical corporations based on the Medical Law

- Auditing of investment business limited partnerships based on the Act on Investment Business Limited Partnership Contracts

- Audit of real estate specified joint enterprise based on the real estate specified joint enterprise law

Voluntary audits Example

- Audit of financial statements based on International Financial Reporting Standards (IFRS)

- Audit of Japanese subsidiaries of foreign companies

- Auditing of subsidiaries of listed companies

- Auditing of SPCs, funds, etc.

- Financial statement audit based on the provisions of the LBO loan agreement

- Auditing of public interest corporations, social welfare corporations, etc.

(Note) As we are not registered as a listed company audit firm, we do not conduct financial statement audits or internal control audits of listed companies based on the Financial Instruments and Exchange Act.

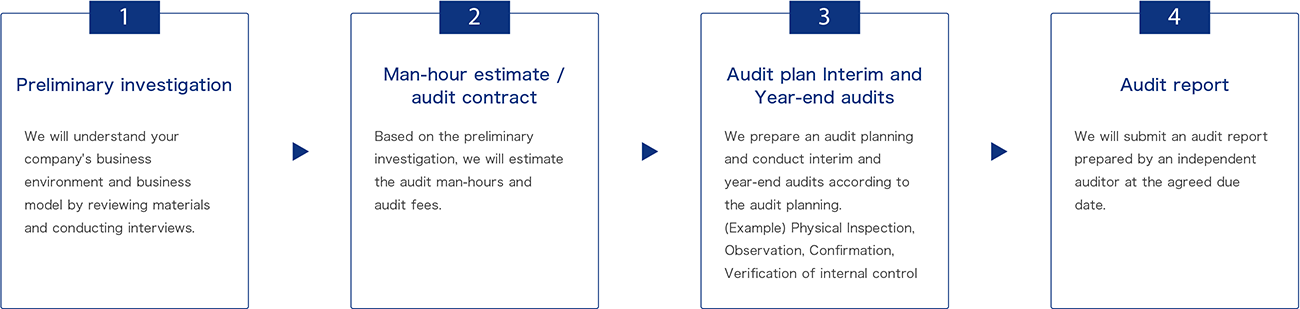

Work Flow

Case of Voluntary audit

Company A

Regarding Company A, a Japanese corporation that is a subsidiary of the Korean listed parent company (listed on KOSDAQ), the parent company requested a voluntary audit to enhance the reliability of the subsidiary's financial statements.

Company B

When issuing a private placement bond, there are cases where a voluntary audit is required at the time of issuance examination by the securities company.

Company C

Company C, which is preparing to go public, requested a voluntary audit in the investment contract with its shareholders in order to ensure the reliability of its financial statements.